Florida Mortgage Lenders For Co-ops

If you are searching for Coop Florida mortgage lenders, Refinance Florida Coop, Jumbo Florida Coop mortgage, or No Tax Return Florida Coop mortgage lenders, then you have come to the right site. When you buy a Florida coop or co-op, you purchase shares in the corporation that owns the co-op. All residents in the building are shareholders, and they all share in the expenses and maintenance of the property. S,o in reality, you are a shareholder in the corporation, versus a typical homeowner. Co-op properties are often funded by private Florida mortgage lenders because Fannie Mae does not purchase co-op loans in Florida.

Florida Coop Mortgage Lenders Refinance Florida Coop

Co-op Florida Mortgage Options Include:

- 30-year fixed

- Up to 80% Loan To Value Up To 1MM

- Minimum 660+ Credit Scores

Co-op Jumbo Florida Mortgage Lenders

- 1,500,000 = 80% LTV

- 2,000,000 = 75% LTV

- 2,500,000 = 70% LTV

- 3,000,000 = 65% LTV

- 3,500,000 = 60% LTV

- 4,000,000 = 55% LTV

- 4,500,000= 50% LTV

- 5,000,000= 50% LTV

Co-op Approval Checklist:

3 documents on checklists to confirm that we can approve the building

Questionnaire – Completed by the managing agent to assess the building’s financial health and suitability for financing.

Master Insurance policy – is a building-wide policy purchased by the co-op or condo association, covering common areas and the building structure.

Budget – Income / Expenses needed to operate and maintain the building, including utilities, insurance, and staff salaries, as well as improvements. following sources of income or employment. Refer to the applicable topics in Chapter B3-3, Income Assessment for additional information about specific tax return requirements.

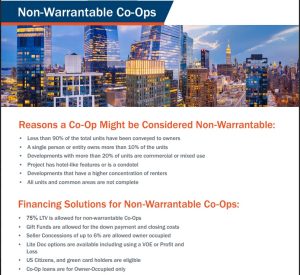

Co-op Restrictions

•Title Insurance policy issued through a title company or closing attorney must be issued on the Co-op certificate.

•Borrower paid attorney review of all applicable co-op documents or other pertinent items required before funding

•Leaseholds allowed with 30 years or more remaining on the lease. Leases with 15 years or more remaining are allowed on investment properties only

Co-op Reserve Requirements:

The current reserve balance meets or exceeds 2 months of the subject property’s HOA dues in reserves multiplied by all units in the project, or 10% or more reserve allocation designated in the most recent budget.

Not allowed:

- NO Co-op Manufactured Homes

- No Structural deficiencies or pending litigation

- Incomplete construction of the subject phase

- Units without a stovetop and oven – must have both

- Homeowners Association with No Reserves

- Homeowners Association limits the number of days the property can be accessed

Co-op Questions And Answers

Q- Does Fannie Mae Buy Co-op loans from lenders in Florida?

A – On the Fannie Mae, it says they will fund loans in Florida, but when I ask Florida mortgage lenders why they don’t make these loans, they say that NO co-ops in Florida meet Fannie Mae’s specifications. This is why most Florida coop loans are harder to come by and are funded only by private non-QM Florida mortgage lenders.

Q – Do we approve loans in coop projects that have resale, age, income, or any other owner-related restrictions?

A – Florida Coop with any sort of resale restrictions presents a severely negative impact on the marketability of the unit in the event the borrower defaults, and this becomes an REO. It is important to identify what the restrictions are to determine project warrantability and eligibility:

- If the only restriction is the “Right of First Refusal”, this is okay, and the project can still be eligible as Warrantable.

- For projects with age restrictions, such as 55-and-older communities, we will allow financing for these projects as long as:

- Borrower meets the age requirements, and;

- The project must not have any rehabilitation, medical treatment, or elder-care facilities (for example, nursing homes).

- The project will only be considered eligible as a Non-Warrantable. If both the above conditions are not met, the loan will be ineligible under all loan programs.

- For projects with income restrictions, such as low-to-moderate income (LMI), we will allow financing to these projects as long as:

- The subject unit is NOT one of the LMI or income-restricted units.

- The project will only be considered eligible as a Non-Warrantable. If the above condition is not met, the loan will be ineligible under all loan programs.

- For all other resale or owner-related restrictions not identified above, the loan will be deemed ineligible under all loan programs.

Q- What Cities Do You Service?

A – All of Florida including and not limited to Jacksonville, Miami, Bal Harbor, Fisher Island, North Bay Village, Hillsboro Beach, Key Biscayne, Fort Lauderdale, Tampa, Palm Beach, Naples, Orlando, St Petersburg, Port St. Lucie, Cape Coral, Tallahassee, Fort Lauderdale, Hallandale, Aventura, Sunny Isles, and all Florida.