Non-Resident Florida Mortgage Lenders Highlights

Non-Permanent Resident Florida Mortgage Lenders program is a unique Housing Empowerment Program in which a purchase transaction is facilitated by an approved non-profit government entity that allows prospective Homebuyers to enter a Structured Financing Agreement to ultimately transition to entering homeownership.

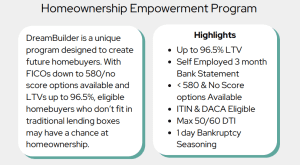

Non-Resident Florida Owner Finance Mortgage Lenders

Owner Finance Matrix

- 5% Downpayment

- Min 580 Credit score

- 1 trade line at least 12 months of history.

- FHA Full Documentation (one year)

- Assets as Income

- Bank Statement Only Income

- 1099s + Bank Statements used for income.

The Homebuyer(s) moves into the property and begins their journey toward owning the home!

• The option purchase price reduces with each monthly payment made by the Homebuyer(s).

• All appreciation acquired from the date of closing until the Homebuyer(s) purchases the property belongs to the

Homebuyer(s).

Step 7: The Homebuyer(s) moves into the property and begins their journey toward owning the home!

• The option purchase price reduces with each monthly payment made by the Homebuyer(s).

• All appreciation acquired from the date of closing until the Homebuyer(s) purchases the property belongs to the

Homebuyer(s).

• At any time, the Homebuyer(s) can sell the home, purchase the property from the eligible government entity, or refinance the loan with a new lender.

Homebuyer Eligibility

• U.S. Citizens

• Permanent Resident Aliens

• Non-Permanent Resident Aliens, including ITIN and DACA

General Owner Finance Program

Can the Homebuyer sell the property that is acquired through the Owner Finance Program?

• The Homebuyer may coordinate the property sale with the government entity (TRHEEA), provided all payments have been timely, the account is in good standing, and the underlying option price is satisfied in full with the property sale.

Otherwise, the Homebuyer must meet all FHA guidelines and assume the FHA mortgage from the government entity,

then the Homebuyer can sell the property after the assumption is complete.

Is the Homebuyer listed on the mortgage security instrument or note?

• No, the Homebuyer is not named on either legal document.

Can the Homebuyer refinance the Owner Finance Program?

• The Homebuyer must first meet all FHA guidelines and assume the FHA mortgage from the government entity. The

Homebuyers can refinance the property after the assumption is completed.

Are seller concessions allowed for the Owner Finance program?

• There are no overlays, refer to the HUD Handbook 4000.1.

Are all title companies approved for the Owner Finance Program?

• No, please refer to the Owner Finance Program Approved Title Company list.

Does the Owner Finance Program have a restriction on the maximum number of Homebuyers for a transaction?

• Yes, no more than four (4) applications are permitted.

Is a non-occupant Homebuyer permitted?

• Yes, refer to the guidelines for details.

Does the Owner Finance Program program allow exceptions?

• Yes, on a case-by-case basis. Refer to the exception parameters of the guidelines for details and requirements.

Owner Finance Credit & Qualifying

What are the tradeline requirements for the Owner Finance Program program? An eligible credit report must reflect at least one (1) tradeline and provide at least 12 months of credit history. Alternative tradeline history may be acceptable, refer to the guidelines for details.

Is a Homebuyer without a credit score acceptable? Yes, Homebuyers without a credit score may be acceptable, subject to the requirements of the guidelines.

What credit bureau is used to qualify for the Owner Finance Program program? At least one (1) credit score from a major bureau is required to qualify. If the Homebuyer has multiple credit scores, the representative score will be the middle score when three (3) credit agency scores return and the lower score when two (2) credit agency scores return. Homebuyers without a credit score may be acceptable, subject to the requirements of the guidelines.

Are Homebuyers with no documented housing history eligible for the Owner Finance Program program? Generally, 12 months of documented payment history (in good standing) is required. Homebuyers who live “rent-free” may be considered on a case-by-case basis, refer to the guidelines.

If the Homebuyer owns their current residence free and clear, can the Owner Finance Program housing payment history requirements be met with a documented history for other real estate owned by the Homebuyer? Yes, housing history for other real estate owned by the Homebuyer will be considered when the primary residence is owned free and clear, subject to validation of reasonable occupancy for the subject property. Additionally, tax and insurance payments for the primary residence will be considered to support a consistent housing history.

What is required if the Homebuyer wants to rent their current primary (departure) residence or has an existing rental property? One (1) currently owned property (departure residence) may be allowed, subject to all requirements of the guidelines. Rental income from an existing rental property may be considered on a case-by-case basis, refer to the guidelines for details.

Do installment debts with less than 10 payments have to be included in the DTI? Yes, in some cases. Refer to the guidelines for details.

Can debt be paid off to qualify? Yes, the assets used for such payoffs must be documented per the guidelines.

If the Homebuyer has tax liens, collections, and/or judgments, how is the debt treated? Generally, a debt payment must be included in the qualifying DTI. Refer to the guidelines for details.

Is it acceptable to exclude self-reported utilities from the DTI? Yes. Utility payments are not required to be included in the qualifying DTI.

Can co-signed debt be excluded from the Homebuyer’s qualifying DTI if documentation supports that another party is paying the debt? There are no overlays, refer to the HUD Handbook 4000.1. Income

Is the income for a self-employed Homebuyer without a business license permitted? May be acceptable on a case-by-case basis.

Will the loan be acceptable if the Social Security Number is different between the Homebuyer’s W-2 and paystubs? Acceptable for ITIN Homebuyers and will be reviewed on a case-by-case basis for all other Homebuyer types.

Can bank statements be used to calculate income for a self-employed Homebuyer? The Owner Finance Program program allows Homebuyers to qualify solely with three (3) months of bank statements when the income source can only be documented with bank statements. For all other self-employed Homebuyers, the Owner Finance Program program requires either prior year tax returns (filed with the IRS), OR a YTD P&L and three (3) months of bank statements to document the business cash-flow, OR K1s and 1120s. Refer to the guidelines for details.

What is the minimum length of self-employment for self-employed income to be acceptable? One (1) year may be acceptable on a case-by-case basis.

Will the income of a self-employed Homebuyer be considered if the tax returns show little to no profit? In some cases, yes, as tax returns are not the only source to validate the Homebuyer’s self-employed income. As a reminder, the Owner Finance Program program requires either prior year tax returns (filed with the IRS), OR a YTD P&L and three(3) months of bank statements to document the business cash flow, OR K1s and 1120s. Refer to the guidelines for details.

What is the age of documentation requirement for a Profit and Loss (P&L) Statement? The P&L must be completed for the most recent quarter as of the Note Date.

If the Homebuyer has more than a single job, for how long must the Homebuyer have the additional job(s) to allow the income to qualify? Less than two (2) years of concurrent employment may be considered on a case-by-case basis.

For employment transfers or relocations, what documentation is acceptable to verify future income?

• There are no overlays, refer to the HUD Handbook 4000.1.